2 Stocks to Avoid in 2024 and Beyond

[ad_1]

The S&P 500 is in a bull market, but some companies aren’t keeping pace. On the one hand, stocks that get left behind during a bull run can be worth investing in, provided they have significant upside potential and their slump is temporary. But other times, companies fail to perform on par with broader equities for a good reason: Serious problems with their businesses are unlikely to be resolved anytime soon. That’s the case with Aurora Cannabis (ACB 6.45%) and Peloton Interactive (PTON 0.44%). Here is why investors should avoid these stocks in 2024 and beyond.

1. Aurora Cannabis

Aurora Cannabis rose in popularity some five years ago when Canada legalized adult use of marijuana. The prevalent opinion was that cannabis sales would skyrocket, and one of the leaders in the field — perhaps Aurora Cannabis — would provide outsize returns to investors who got in early. However, things haven’t worked out that way. The Canadian cannabis market suffered from oversupply and an incredibly slow process to obtain retail licenses.

Meanwhile, Aurora Cannabis’ efforts were not very successful. The company tried to secure a partner with deep pockets, ideally one in a tangentially related industry. Some of its peers — namely, Canopy Growth and Cronos Group — were able to pull that off, but Aurora Cannabis failed in its quest. The company also resorted to an aggressive growth-by-acquisition strategy, which was funded by issuing new shares, thereby diluting existing shareholders.

The results have been inconsistent revenue, persistent net losses, and terrible stock market performance. Some might say that this is in the past and isn’t relevant to Aurora’s future performance. That’s hardly the case.

For one, challenges remain in the Canadian marijuana market. It is still ruthlessly competitive. Aurora Cannabis is currently seeing some success in the medical marijuana space, but many of its peers are pouncing on this opportunity, which, by the way, is much smaller than the recreational market. So it is unlikely to produce significant growth for Aurora Cannabis for a while.

The pot grower is also trying to make a splash in the market for cannabis-infused beverages. That’s another area where many of its rivals — including the leading marijuana specialist in Canada, Tilray — are trying to salvage their failing businesses.

Aurora Cannabis promised to deliver positive free cash flow in 2024. Even if the company achieves that goal, given its poor track record, the challenges in the marijuana market, and the lack of a stable and reliable growth vision, investors should completely ignore the stock.

2. Peloton Interactive

Peloton’s fitness offerings were a hit during the early days of the COVID-19 pandemic. As gyms closed due to government-imposed lockdown orders, people rushed to buy the company’s exercise bikes and treadmills, allowing them to stay active. Peloton was all the more appealing because of the classes it offers through its subscription services. But that business model crumbled once gyms started reopening. Peloton’s equipment is pricey even beyond the subscription. Plus, many people were sick of staying home.

The company’s results have been subpar (at best) for the past couple of years, with declining revenue, persistent net losses, dropping subscription numbers, and a catastrophically lousy performance in the stock market.

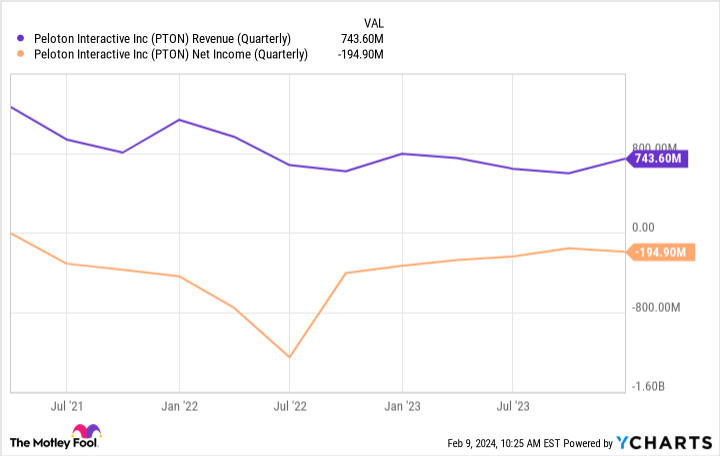

PTON Revenue (Quarterly) data by YCharts.

Is there any hope for Peloton? The company is increasingly looking to switch to the subscription model, which carries much juicier margins. In the second quarter of its fiscal 2024 (which ended on Dec. 31, 2023), Peloton’s revenue of $743.6 million fell by 6% year over year. However, subscription revenue rose 3% year over year to $424.5 million. That’s not particularly impressive, but it’s much better than the company’s overall sales growth.

Furthermore, subscription gross margin was 67.3%, slightly lower than the year-ago period. Peloton’s total gross margin came in at a much lower 40.3%. The company also improved its net loss and free cash flow.

However, there is a long road ahead for Peloton before it can fully recover; in my view, there is a good chance it will never get there. It faces competition from other companies with similar business models, but they often offer lower prices. And gyms remain a thing, of course. They, too, are much cheaper than what Peloton offers.

So while Peloton has made some progress, the company may never attract the clientele it needs — or at least a large enough percentage thereof — to complete its turnaround. That’s why it’s best to stay away from the stock.

[ad_2]