Hormel Foods: Buy, Sell, or Hold?

[ad_1]

The food company is trying to get back on its feet after some trying years.

Food products company Hormel Foods (HRL -0.06%) could be considered a blue chip stock. Most companies that raise their dividends every year for more than five consecutive decades earn that label. But Hormel’s stock price doesn’t reflect that now — it’s down nearly 40% from the all-time high it reached two years ago.

Investing in broken blue chip companies can be a lucrative long-term strategy if their struggles relate to temporary issues. Hormel has been dealing with cost pressures that have dragged its margins lower and hurt earnings growth.

Should investors buy the stock, hold it if they already own it, or avoid it altogether?

Persistent struggles

No company avoids adversity forever. However, Hormel has been dealt an unusually tough hand repeatedly over the past decade.

The food products company has heavy exposure to poultry and pork due to its turkey business and pork-based products like lunch meats, pepperoni, and proteins. Volatile commodity prices for poultry and pork can disrupt its business. Between 2018 and 2023, Hormel grappled with outbreaks of both swine fever and bird flu, as well as the operating restrictions and end-market quirks that came with the COVID-19 pandemic.

All of these events disrupted Hormel’s core commodity markets and supply chains, impacting its sales volumes. The financial hit was noticeable, and higher-than-usual inflation over the past three years has further increased its costs.

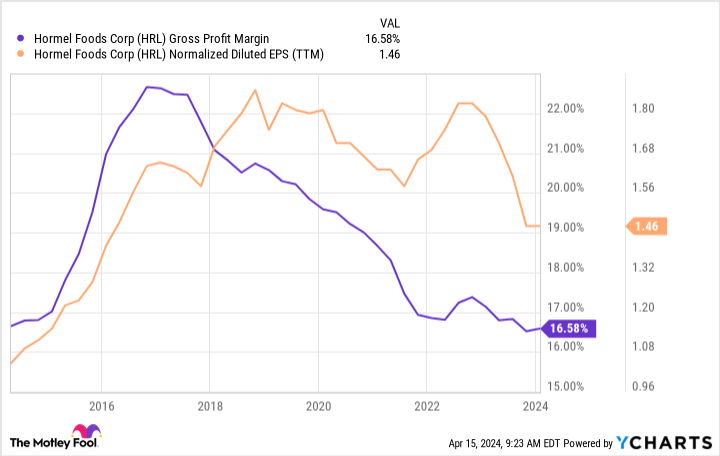

Gross profit margins have slipped significantly from 2017 levels, and earnings per share have declined to levels last seen in 2016.

HRL Gross Profit Margin data by YCharts.

These issues aren’t Hormel’s fault, but it’s clear that the company hasn’t been able to offset these challenges. The business has deteriorated. Hormel made a big splash in 2021 by acquiring the Planters snack brand for $3.3 billion, but that hasn’t stopped earnings from declining, and the deal put more debt on its balance sheet.

Is the dividend safe?

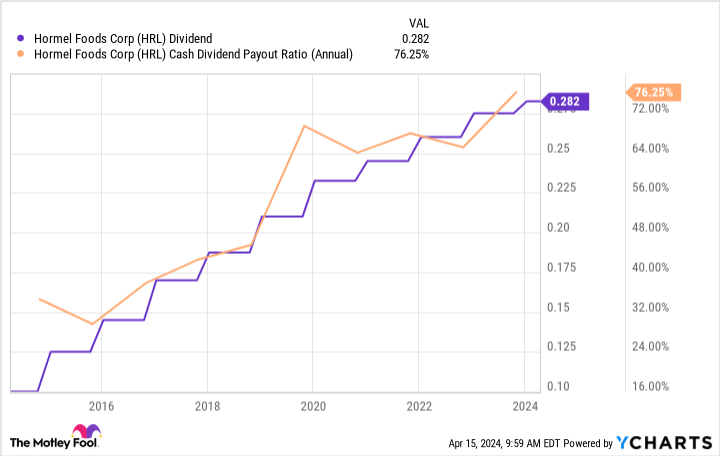

It’s not all bad news. After all, companies don’t become Dividend Kings by accident, and Hormel has continued to boost its dividend despite its struggles. However, in recent years, Hormel has arguably leaned too heavily on dividend increases. The payout has nearly doubled over the past decade, pushing the payout ratio to over 76% of free cash flows.

HRL Dividend data by YCharts.

Investors shouldn’t fear a cut at this point, though. Hormel’s dividend-raising reputation is in its DNA, and it would take an existential crisis to force a cut. I don’t think the company is in such dire straits. Its balance sheet is still healthy, leveraged to a manageable 2.4 times its EBITDA. Investors shouldn’t worry too much unless the payout ratio exceeds 100%.

Is Hormel a buy, sell, or hold?

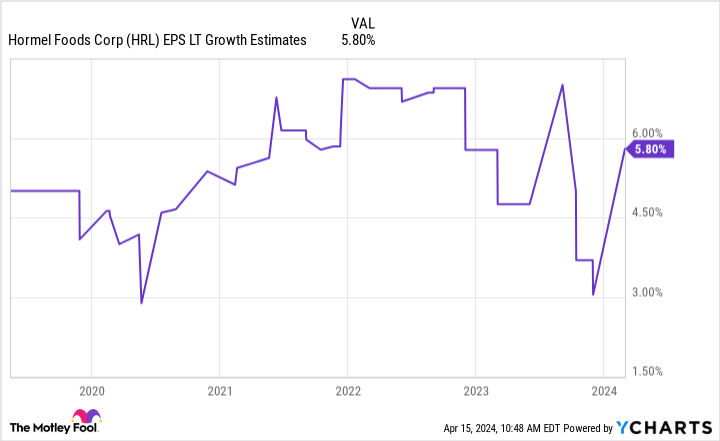

Hormel is optimizing its operations, which management believes could free up $250 million in annual savings that would fall straight to operating income. I previously wrote about how that could boost earnings beyond the mid-single-digit percentage annualized growth analysts expect over the next three to five years.

However, execution is never guaranteed, and the stock now trades at more than 21 times the company’s estimated 2024 earnings. That’s a steep valuation if Hormel doesn’t outgrow analysts’ expectations.

HRL EPS LT Growth Estimates data by YCharts.

So what’s the final verdict?

I believe Hormel’s anticipated cost savings will boost cash flow and decrease its dividend payout ratio. Additionally, investors are getting a hefty 3.3% dividend yield with a 58-year track record of growth while they wait for the business to rebound.

But with the share price a tad higher than it was months ago, there’s not as much margin of safety in the stock today. To me, that makes Hormel a hold.

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

[ad_2]