Is Baytex the Best Oil Stock to Buy Right Now?

[ad_1]

The stock has the potential to move significantly higher if energy prices remain elevated.

Shares of oil producer Baytex (BTE -1.57%) have largely been range-bound over the past year. However, the stock could be one of the best plays on high oil prices around.

Let’s examine why oil bulls should consider buying the stock right now.

Transformative acquisition

Baytex operates both in the U.S. and Canada, producing both light and heavy crude, as well as associated natural gas and natural gas liquids (NGLs). About 84% of its production is liquids.

The company primarily operated in Canada until last year, when it acquired Ranger Oil, which operated in the Eagle Ford in Texas. Baytex had a small non-operated position in the Eagle Ford at the time, so it was familiar with the basin. It paid $2.2 billion in cash and stock for Ranger in a deal that transformed the company: Now, more than 60% of Baytex’s production comes from the Eagle Ford.

The Eagle Ford will be Baytex’s biggest growth driver as well, with over 60% of its capital expenditures being directed toward the basin. The company is looking to grow its overall production by a steady 1% to 4% a year through 2028.

The big advantage of the Eagle Ford over Baytex’s other assets is that it gets premium U.S. Gulf Coast pricing. Canadian oil often trades at a discount to the West Texas Intermediate (WTI) benchmark that is typically quoted in the U.S. Following the Ranger acquisition, more than 40% of the company’s liquid production received WTI equivalent pricing in Q4.

Deleveraging opportunity

In order to purchase Ranger, Baytex took on additional debt and ended 2023 with 2.5 billion Canadian dollars ($1.9 billion) in net debt. While its year-end leverage (net debt/adjusted EBITDA) was only 1.1 times, the price of oil can have a big influence on its leverage metric, as the company would generate much less EBITDA in a lower oil price environment. As such, the company is looking to reduce its debt to CA$1.5 billion ($1.1 billion) in the coming years.

Image source: Getty Images

Baytex has projected that it will generate CA$530 million ($388 million) in free cash flow in 2024. It said it planned to spend half of that on debt reduction and the other half on stock buybacks and dividends.

Importantly, though, those projections were based on a WTI price of $73 per barrel. Today, WTI is sitting around $85. The company noted that a $5 change in WTI would add CA$215 million ($157 million) to its annual cash flow. In addition, the company was using a heavy oil differential (the difference in price between Canadian oil and WTI) of $16, while today, the differential is around $12. Management said that every $1 improvement in that differential would positively impact cash flow by CA$15 million ($11 million) a year.

At current WTI prices and differentials, Baytex would be able to generate around CA$1 billion ($733 million) in free cash flow. That would allow it to pay down its debt much more quickly than previously envisioned, as well as buy back more stock. Both should help drive the stock higher.

A cheap stock

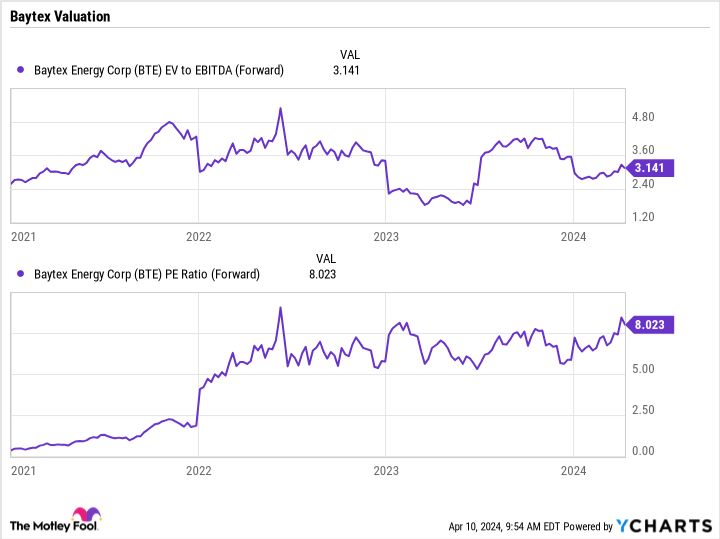

Baytex’s stock trades at attractive valuations, with an enterprise-value-to-adjusted EBITDA ratio of just over 3 and a forward price-to-earnings ratio of around 8. The former metric takes into consideration the company’s debt, but factors out non-cash items and interest expenses.

BTE EV to EBITDA (Forward) data by YCharts.

It is also notable that buying back stock shrinks the numerator in the equations (market cap and enterprise value) for both metrics, while paying down debt lowers its enterprise value. In that scenario, in order for the company to just maintain its current valuation levels, the stock would have to move higher.

As the company pays down debt, though, it should be able to command a higher multiple. Given the strong cash flow Baytex will generate at current oil prices, that should happen fairly quickly. This combination creates a lot of upside potential and is why Baytex is one of the best oil stocks to buy right now.

[ad_2]