Mastercard: Buy, Sell, or Hold?

[ad_1]

Mastercard (NYSE: MA) has been a standout stock for investors since it went public in 2006, and it has delivered market-crushing returns. In fact, if you invested $10,000 in the company at that time, you would have over $11 million today.

Mastercard has a distinct advantage that has made it a stellar long-term performer. Its role as one of the largest payment networks positions it to capture further market share in emerging economies while adapting to new technologies.

Here’s what you need to know if you plan on buying the stock.

Mastercard’s competitive advantage

Mastercard helps facilitate payments globally through its debit cards, credit cards, and other payment methods. With over $9 trillion in purchase and cash volume in 2023, it is the second-largest payment network in the U.S., behind Visa.

What makes Mastercard compelling are the strong network effects around its business, which have taken years to build up. It’s a key player in coordinating money movement from banks to customers to merchants worldwide.

Payment processing isn’t an easy industry to break into. Companies like Mastercard and Visa benefit from brand recognition and a network that people trust. And these companies invest heavily in technological infrastructure to deal with issues like regulatory requirements, security, and fraud prevention.

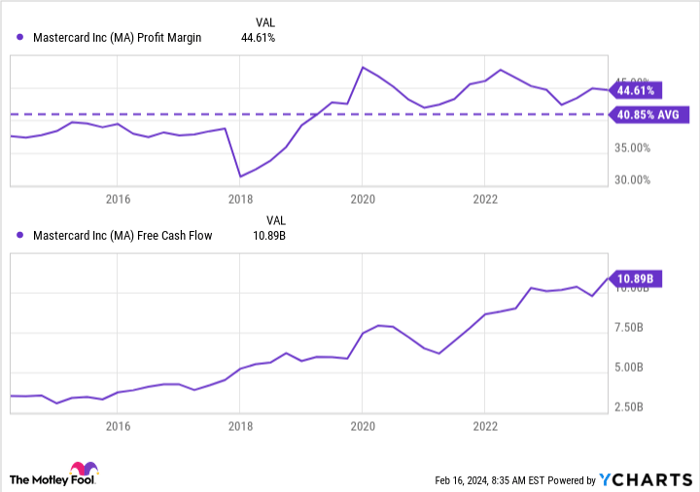

One way Mastercard’s competitive advantage is evident is by looking at its margins. Over the past decade, its profit margin has averaged a very healthy 41%. These margins mean lots of free cash flow, and they produced over $10.9 billion last year. This is cash the company can use to invest in the business, buy back shares, and pay to investors through dividends.

MA profit margin data by YCharts.

Here’s why Mastercard could weather a spending slowdown

Last year’s spending volume remained very healthy. It increased significantly on cross-border transactions, up 24% year over year. Total volume increased 12%, while revenue and net income grew by 13% from the prior year.

Mastercard should continue to do well in 2024, although there is the potential that spending could slow down. Many economists had predicted a slowdown last year, which has failed to materialize. However, higher interest rates could weigh on consumer spending.

Jack Kleinhenz, chief economist at the National Retail Federation, said in a note that “maintaining the recent pace of growth will be increasingly difficult” for consumers. But despite the potential for a slowdown, analysts expect Mastercard’s revenue and earnings per share to grow by 12% and 17.5%, respectively, in 2024.

Another thing bank investors are watchful of is credit quality. However, one benefit Mastercard has over companies like American Express and Discover Financial Services is that it doesn’t hold any loans on its books from credit cards or other sources. Instead, it focuses on facilitating payments, while banks and other partners are responsible for servicing the debt. So, while spending could take a hit, it’s not vulnerable to credit losses.

Image source: Getty Images.

Is it a buy?

Mastercard is well positioned for ongoing tailwinds in digital payments, growing e-commerce trends, and expansion across emerging markets. According to Statista, the global digital payments market is projected to expand to $16.6 trillion by 2028, an annual growth rate of 9.5%.

And the company continues to innovate. One thing it’s been working on is using artificial intelligence (AI) to scan and evaluate 1 trillion data points to predict whether a transaction is genuine. According to the company, AI enhancements boost fraud detection by 20% on average, allowing banks to better protect their cardholders.

Mastercard stock is up 25% from November but still trades at a reasonable valuation compared to its recent history. Today, the stock is priced at 39.8 times earnings, slightly above its 10-year average of 37.5. Given the company’s strong position in the payment space and its runway for future growth, I give it a buy rating today.

Should you invest $1,000 in Mastercard right now?

Before you buy stock in Mastercard, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Mastercard wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

See the 10 stocks

*Stock Advisor returns as of February 12, 2024

American Express is an advertising partner of The Ascent, a Motley Fool company. Discover Financial Services is an advertising partner of The Ascent, a Motley Fool company. Courtney Carlsen has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Mastercard and Visa. The Motley Fool recommends Discover Financial Services and recommends the following options: long January 2025 $370 calls on Mastercard and short January 2025 $380 calls on Mastercard. The Motley Fool has a disclosure policy.

[ad_2]