Why Upstart Stock Jumped 53% in December

[ad_1]

Shares of lending-technology company Upstart (UPST -10.28%) jumped 52.7% in December, according to data provided by S&P Global Market Intelligence. As much as the bulls might want to celebrate, the reality is that the company’s recent stock performance appears more related to commentary from the Federal Reserve than factors within the business itself.

In December, the Federal Reserve opted to hold interest rates steady. And commentary from members of the committee strongly suggests that rates could get lowered three times this year, which would potentially be good for Upstart’s business.

Why do rates matter for Upstart?

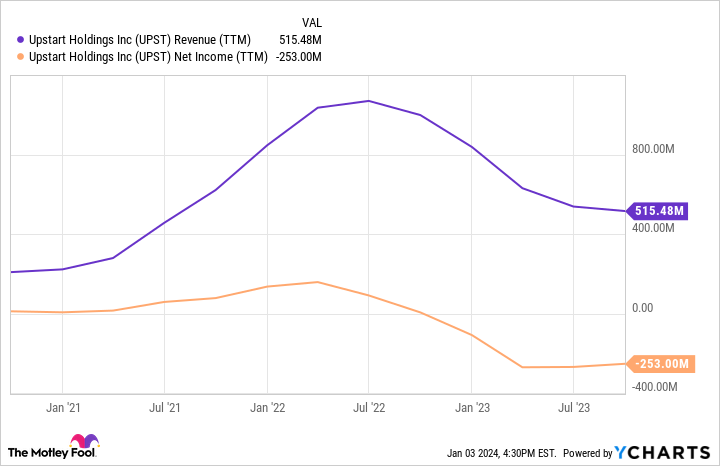

Upstart has developed its own system that it hopes will replace the credit score. The company partners with banks and credit unions to approve more credit-worthy borrowers and provide better rates, and in return the lenders hopefully get fewer delinquencies.

When interest rates are elevated, like now, less money is available to fund loans — investors would rather put more money in high-yield, risk-free opportunities. Moreover, borrowers aren’t as eager to take on debt at higher rates. Both of these factors result in Upstart’s software processing fewer loans.

As a result, Upstart’s revenue has dropped and its profits have turned into losses, as the chart below shows.

UPST Revenue (TTM) data by YCharts

The hope is that the Federal Reserve will lower rates in 2024 and that Upstart’s business will consequently get back on track. That’s why Upstart stock was up in December.

Not so fast

As of this writing, we are only two days into the new year, and Upstart stock is already down 15%. In large part, the stock is down because the minutes from the Federal Reserve came out, and it seems that the potential rate cuts in 2024 are far from a done deal. Rates could potentially hold steady.

It’s a good reminder that investors should always take macroeconomic predictions such as interest rate cuts with a grain of salt. No one fully knows what will happen in the next year, not even the decisionmakers at the Federal Reserve. Therefore, investors can’t build an investment thesis for Upstart stock based solely on this factor.

Upstart started out with personal loans but more recently has expanded into auto loans and home equity lines of credit. This expansion could eventually provide an explosive revenue growth opportunity. However, even with this recent expansion, loan volumes are still down for the company.

For now, I still see reason to hold Upstart stock. One key metric for its long-term adoption is its partners. It has over 100 bank and credit union partners today compared with just 10 three years ago. Therefore, this business still holds long-term promise for patient investors.

Jon Quast has positions in Upstart. The Motley Fool has positions in and recommends Upstart. The Motley Fool has a disclosure policy.

[ad_2]